Investment Market Update

SEPTEMBER 2024

What developments have unfolded in local and global markets throughout the month of September?

R17.1

R17.1

The rand’s monthly low against the dollar

R21.4

R21.4

Petrol reaches its lowest in over a year

21%

21%

China’s CSI 300 return for September

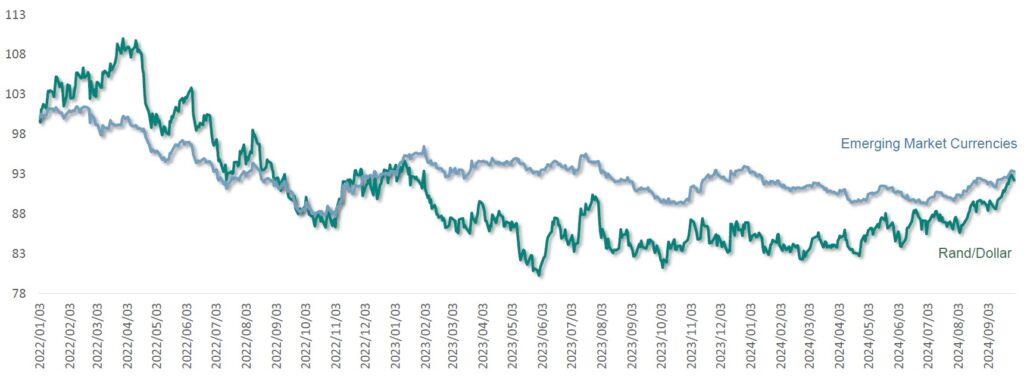

EMERGING MARKETS VS THE RAND

EMERGING MARKETS VS THE RAND

US DOLLAR VS THE RAND

US DOLLAR VS THE RAND

EMERGING MARKET EXCHANGE RATE VS USD

EMERGING MARKET EXCHANGE RATE VS USD

GLOBAL MARKET

_______________________

In September, several central banks lowered interest rates as expected, signaling a global shift in monetary policy for varying reasons. The US Federal Reserve surprised markets by cutting rates by 0.5% instead of the anticipated 0.25%.

ANALYTICS SEPTEMBER COMMENTARY:

SMARTIE BOX IN RANDS:

LOCAL MARKETS

__________________________

South African asset classes benefited significantly from global macroeconomic trends in September. A rally in China’s equity markets, driven by a government stimulus package, lifted local markets, particularly in resources and industrials.

The South African Reserve Bank (SARB) also cut interest rates by 0.25%, which supported bonds, and the Rand strengthened against major currencies as the SARB’s rate cut was smaller than the US Federal Reserve’s.

Positive local developments further boosted sentiment. Inflation eased for the third consecutive month, falling to just below 4.5%, and South Africa marked 188 days without loadshedding. The SARB lowered its lending rate to 8.0%, its first cut in over four years, while maintaining a cautious outlook on inflation risks. The rate cut, along with China’s policy support, improved domestic sentiment and led to a strong performance in South African equities, with the Retail and Industrial sectors leading the way. Heavyweights like BHP Group, Prosus, and Naspers posted impressive gains. However, Sasol and Aspen lagged.

South African bonds saw their sixth consecutive positive month, supported by the stronger Rand and increased foreign buying. The Rand appreciated nearly 6% against the US dollar and 5% against the euro for the year. Meanwhile, gold reached a new high, ending September almost 28% higher since January, while oil prices dropped by 8.9% during the month.

- The JSE All Share Index soared higher (up 4.0%) closing out an already successful quarter on a high note.

- The local bourse was supported by all three major sectors, as Financials (up 2.5%), Industrials (up 5.2%) and Resources (up 3.9%) all gained ground.

- Small-caps (up 4.0%), Mid-caps (up 5.1%), and Large-caps (up 3.7%) all advanced to higher levels.

- The S&P SA REIT sector (up 5.5%) and the SA Listed Property sector (up 5.0%) continued to perform well and closed out the quarter as the best performing local asset classes.

- SA Nominal Bonds (up 3.9%) saw large gains after the SARB cut interest rates, and Inflation Linked Bonds (up 0.9%) inched higher as inflation slowed.

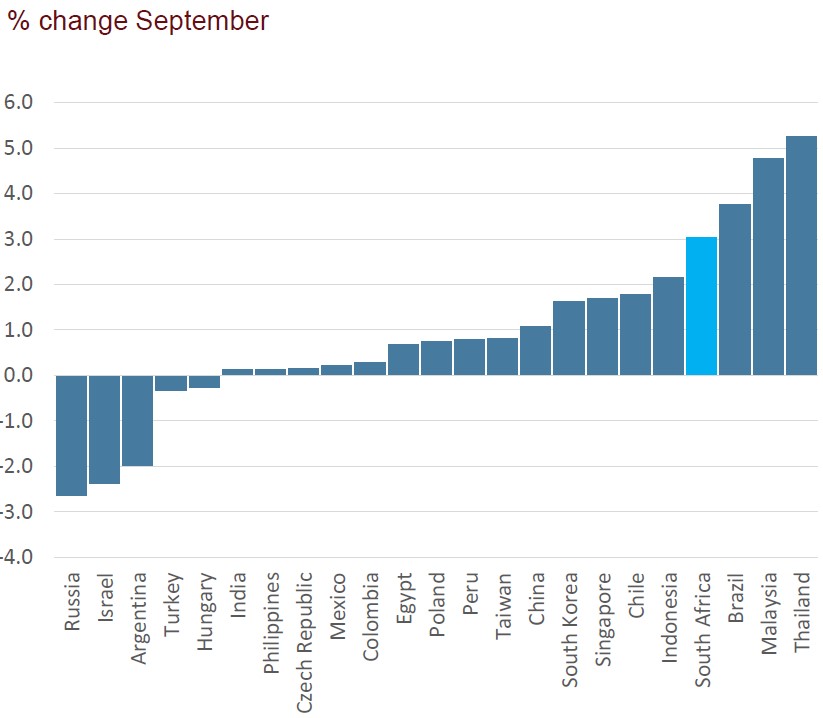

- Developed Market Equities were left in the dust by their Emerging Market peers in US Dollar terms, with the MSCI World Index up only 1.9% as the MSCI Emerging Market Index recorded massive gains, adding 6.7%.

- The Rand had another strong month, despite local rate cuts. Relative to the US Dollar (Rand appreciated 2.9%), the Euro (Rand appreciated 2.1%) and the Pound Sterling (Rand appreciated 0.9%).

- Commodities were mostly positive in September. Gold (up 5.7%) and Platinum (up 5.5%) rallied hard, as Brent Crude (down 8.9%) dropped sharply.

MONTHLY RETURNS: